Iran, the Strait of Hormuz, and What the Latest Disruption Means for Japan

Key takeaways

Japan is highly exposed to disruption in the Strait of Hormuz because it remains heavily dependent on imported fossil fuels from the Middle East.

The most likely near-term impact is not only higher energy and shipping costs, but also broader inflationary pressure across the Japanese economy, with knock-on effects for electricity, gas, transport, consumer goods, and industrial supply chains.

The crisis is likely to strengthen Japan’s push for greater energy security through supply diversification, stronger international partnerships, and more focus on domestic power sources such as nuclear and renewables.

The latest conflict involving Iran and the severe disruption to shipping through the Strait of Hormuz has once again brought energy security to the forefront of Japan’s policy debate. While headlines often focus on Iran itself, the real issue for Japan is broader. The Strait of Hormuz is one of the world’s most important energy chokepoints, and Japan remains heavily dependent on imported fossil fuels from the Middle East that pass through it. That means instability in the strait can quickly become a Japanese economic, industrial, and strategic problem.

This matters not only for crude oil prices, but for the overall resilience of Japan’s economy. The latest data suggests the immediate effects are already visible in global markets. The larger question is what prolonged disruption would mean for Japan over the coming weeks and months.

The U.S. Energy Information Administration estimates that only around 2.6 million barrels per day of Saudi and UAE pipeline capacity could be available to bypass the strait during a disruption, versus nearly 20 million barrels per day of oil exports that normally transit Hormuz. In other words, they provide only partial relief, not a full substitute, in a serious disruption.

The Strait of Hormuz is a global chokepoint

The Strait of Hormuz is one of the world’s most critical maritime corridors for energy trade. The International Energy Agency says an average of 20 million barrels per day of crude oil and oil products moved through the strait in 2025, equivalent to roughly one-quarter of global seaborne oil trade. It also says more than 110 billion cubic meters (bcm) of LNG passed through the strait in 2025, representing nearly one-fifth of global LNG trade.

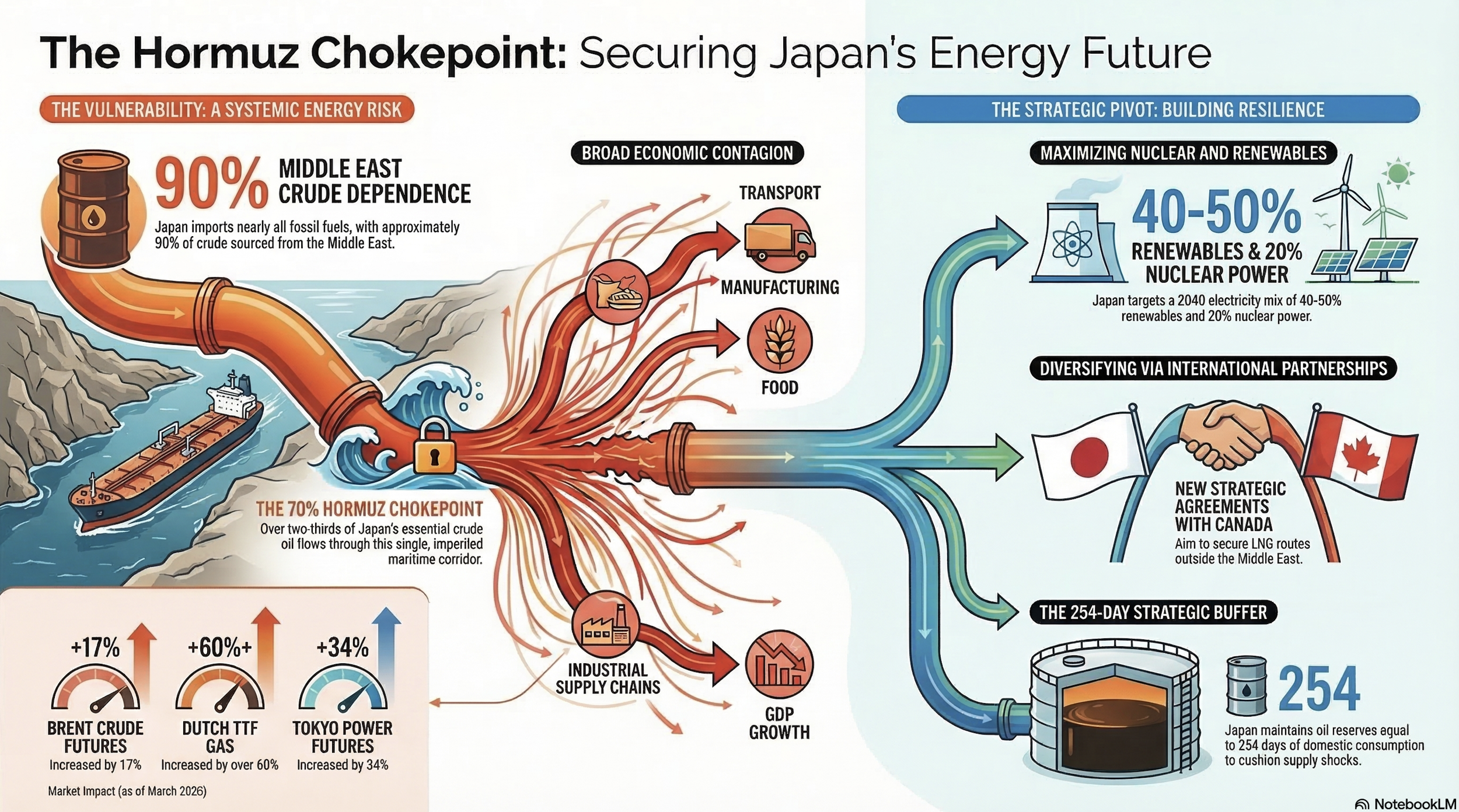

The latest disruption has already had market consequences. According to the IEA, some operators have begun shutting in production, while refined products and LNG output have also been significantly affected. The agency says Brent crude futures rose 17% through March 5, and Dutch TTF gas rose by more than 60% since the start of hostilities. For Japan, the impact is already showing up in domestic energy markets. Bloomberg reports that Japanese power futures jumped as traders moved to hedge against tighter LNG supply and higher fuel costs, with the FY2026 baseload Tokyo contract on the European Energy Exchange rising to ¥16.38/kWh, up 34% since the previous Friday. A Nomura Research Institute report noted that should crude oil prices rise by about 30 percent, Japan’s real GDP would decline by an annualized 0.18% while further contributing to inflation. BOJ Governor Kazuo Ueda has also warned that the conflict could have a significant impact on Japan’s economy through higher energy prices and financial-market effects.

There are only limited alternatives if Hormuz traffic remains constrained. The U.S. Energy Information Administration estimates that only around 4.7 million barrels per day of Saudi and UAE pipeline capacity could be available to bypass the strait during a disruption. That is far below the normal volume that transits Hormuz, which means rerouting options are limited in a serious crisis.

Iran’s exports show this is not just an oil issue

Iran remains an important exporter of crude and condensate, but its export profile also reveals wider supply chain risks. EIA estimates Iran’s crude oil and condensate exports rose from 1.327 million barrels per day in 2023 to 1.483 million barrels per day in 2024, generating about $43 billion in revenue. It also estimates that 1.444 million barrels per day of those exports went to China, showing that Iran’s crude trade is now overwhelmingly China-oriented.

For Japan, however, the bigger issue is not direct dependence on Iranian crude. It is the fact that the same chokepoint is essential for energy exports from Saudi Arabia, the UAE, Kuwait, Qatar, Iraq, Bahrain, and Iran. In other words, Japan’s vulnerability within the Middle East is systemic.

Iran’s broader trade profile also matters. WTO data shows that in 2024 Iran’s leading exports included LNG at $6.44 billion, liquefied propane at $3.25 billion, methanol at $2.30 billion, petroleum bitumen at $2.17 billion, liquefied butanes at $2.07 billion, urea at $1.74 billion, and significant volumes of polyethylene. These product categories are important because they feed into chemicals, plastics, construction materials, fertilizers, packaging, and industrial manufacturing.

Disruption centered on Iran and Hormuz should not be understood solely as a crude oil problem. Risks have skyrocketed for petrochemical supply chains, industrial feedstocks, and broader trade flows across Asia.

Why Japan is especially exposed

Japan’s exposure to this kind of disruption remains high. A METI presentation from 2025 notes that Japan imports almost all of its fossil fuels from abroad and that crude oil dependence on the Middle East is approximately 90%. It also shows that in FY2023 Japan’s crude oil input came primarily from Saudi Arabia at 40.8%, the UAE at 39.6%, Kuwait at 9.0%, and Qatar at 4.7%. Around 70% of this crude oil flows through the imperiled Strait of Hormuz.

Recent monthly data points in the same direction. AP, citing METI, reports that Japan imported about 2.34 million barrels per day of crude in January 2026, around 95% of it from the Middle East.

Japan’s LNG supply is somewhat more diversified than its oil supply, but the risk is still material. METI’s data shows Qatar accounted for 4.4% of Japan’s LNG input in FY2023. EIA also estimates that 83% of LNG moving through Hormuz in 2024 went to Asian markets. Any prolonged disruption will tighten LNG availability and pricing across Asia, even for countries that are not overwhelmingly dependent on Qatari gas itself.

This is the core point for Japan. The country does not need to be a major direct buyer of Iranian crude to feel the consequences of an Iran-related Hormuz crisis. Its dependence on the Gulf energy system is enough.

Implications for Japan’s energy security

Likely economic and industrial impacts on Japan

The most immediate likely consequence is higher energy costs. If over 90% of Japan’s crude oil still comes from the Middle East, and if global oil and gas prices are already rising because of the disruption, then upward pressure on electricity, gas, transport, and industrial fuel costs is a logical expectation. The precise speed of pass-through depends on utility pricing structures, government subsidies, and contract timing, but the directional pressure is clear.

A second likely consequence is broader inflationary pressure across the Japanese economy. If higher oil, LNG, electricity, shipping, and insurance costs persist, those increases are likely to be passed through into a wider range of goods and services over time. This is a logical expectation given Japan’s high dependence on imported energy from the Middle East and the central role of shipping and fuel costs in industrial production, logistics, food distribution, and consumer goods. As noted above, the Bank of Japan has stated that higher oil prices present a two-sided inflation risk: they could suppress underlying inflation by dragging on economic activity and worsening the terms of trade, or amplify it by entrenching higher price expectations if the rise is sustained. The impact of a prolonged Hormuz disruption may not be limited to utilities or heavy industry, but could also contribute to higher prices more generally across transport, household goods, food-related supply chains, and other everyday expenses.

A third likely consequence is supply chain disruption. Iran’s export mix includes methanol, liquefied hydrocarbons, bitumen, and polyethylene, while the wider Gulf region is a major source of refined fuels and petrochemical inputs. The IEA has already warned that refined products and LNG output have been significantly affected, and that diesel and jet fuel markets are under particular strain. Domestic ethylene producers have either reduced production or have told business partners that they may halt operations due to the lack of naphtha, a byproduct of crude oil refinement necessary for the manufacturing of ethylene. The chemical is a plastic ingredient used in a wide range of Japanese industries, illustrating the knock-on effects to broader supply chain disruptions. For Japan, the disruption in trade creates a credible pathway to higher costs and tighter supply for plastics, packaging, chemicals, logistics, aviation, and some manufacturing processes.

Wider geopolitical implications for Japan

The latest Hormuz disruption is also likely to reinforce broader shifts already underway in Japan’s national strategy. In Tokyo’s view, energy insecurity, economic security, and defense policy are becoming more interconnected. Japan’s Seventh Strategic Energy Plan, approved by the Cabinet in February 2025, explicitly links energy policy to geopolitical instability and the need for a more resilient supply-demand structure. It states that Japan should maximize renewable energy and nuclear power while improving overall energy self-sufficiency.

One logical implication is greater pressure to sustain and potentially increase defense spending. This trend was already underway before the latest crisis. Japan’s Ministry of Defense says the government brought forward its goal of reaching defense spending equivalent to 2% of GDP by FY2025, citing an increasingly severe security environment. Previous governments have debated whether minesweeping the Strait of Hormuz would classify as a “survival-threatening situation” that would trigger the deployment of the Japan Self-Defense Forces (JSDF), but as of the publication of this report Prime Minister Takaichi has stated that she does not believe the current conditions have escalated to that level. As this situation develops, we are also likely to see broader defense discussions tie in with Japan’s ongoing legal and constitutional debate. This crisis is likely to reinforce an existing trajectory toward stronger operational capabilities and a more expansive national security debate.

More diversification through international partnerships

Another likely effect is a stronger push to diversify energy supply through international partnerships. This is not hypothetical. It is already visible in recent diplomacy. Japan and Canada have signed a new strategic agreement covering defense, economic security, and energy security, with both sides highlighting the importance of securing and diversifying energy resources amid the latest Middle East tensions. This builds on broader Japan-Canada cooperation. In October 2025, METI and Natural Resources Canada issued a joint statement saying additional LNG projects on Canada’s west coast could support Japan’s energy security and help Asian markets deal with geopolitical supply risks. Canadian LNG is especially relevant because it offers Japan a route to reduce marginal dependence on Middle Eastern supply and on Hormuz-linked disruptions over time.

Why renewable energy and nuclear policy is likely to become even more important

One of the clearest implications of this crisis is that it strengthens the policy case for energy sources that reduce Japan’s reliance on imported fossil fuels. Japan’s current Strategic Energy Plan targets a future FY2040 electricity mix with 40-50% renewables and around 20% nuclear, explicitly linking those goals to energy security.

That makes stronger momentum behind nuclear restarts a logical prediction. If Japan remains heavily exposed to imported fossil fuels moving through unstable regions, then restarting already approved nuclear reactors becomes easier to justify from an energy security perspective. This goes hand in hand with the government’s push to adopt renewables, as the official strategy is to maximize both renewables and nuclear power. But the Hormuz disruption adds urgency to the argument that Japan needs more domestically available and geopolitically insulated power sources that can be deployed within a relatively short timeline.

Japan has buffers, but not immunity

Japan does have important short-term buffers. As of the end of December 2025, Japan had oil reserves equal to 254 days of domestic consumption. Those reserves provide Japan with a substantial cushion against an immediate physical supply shock, even as the government reportedly prepares for the possibility of releasing part of its national stockpile if disruption in the Strait of Hormuz is prolonged.

Still, stockpiles buy time, not immunity. They do not prevent global benchmark prices from rising, nor do they eliminate tighter LNG markets, higher shipping costs, or broader industrial disruption if Hormuz remains impaired for an extended period. The real issue for Japan is therefore not whether it has emergency reserves, but whether the disruption is short-lived or prolonged.

Conclusion

The latest Iran-related disruption in the Strait of Hormuz is a reminder of a structural reality Japan has long lived with: its economy still depends heavily on imported energy moving through geopolitically sensitive routes. Japan’s import structure shows just how exposed it remains to Gulf-centered supply shocks.

The most defensible prediction is not panic, but pressure. Pressure on import costs. Pressure on electricity and gas prices. Pressure on plastics, chemicals, transport, and industrial supply chains. Pressure on Japan to keep strengthening defense and economic-security policy. Pressure to deepen partnerships with countries like Canada that can help diversify supply. And pressure to accelerate domestic sources of stable power, particularly nuclear restarts alongside renewables and efficiency improvements.

If you found this overview useful and want more regular insights into Japan’s politics and public policy, sign up to our mailing list and stay ahead of the developments shaping Japan’s future.

Frequently Asked Questions (FAQ)

Q: Which Japanese industries face the most immediate supply chain risk beyond energy?

A: Beyond utilities and refiners, the most immediate industrial exposure is likely in chemicals and materials that depend on oil-derived feedstocks and refined-product markets, including plastics, packaging, and some manufacturing inputs. Aviation is also exposed due to jet-fuel markets are already under strain. If disruption persists, higher shipping, fuel, and insurance costs would then spread more broadly across logistics-intensive sectors such as autos, electronics, food distribution, and construction materials.

Q: How realistic is Canadian LNG as a near-term alternative for Japan?

A: Canadian LNG is now more realistic than it was a year ago, because LNG Canada began exporting in June 2025. But it is still not a near-term substitute on the scale needed to offset a major Hormuz disruption. In practice, Canada is better understood as part of Japan’s medium-term diversification strategy rather than an immediate relief valve.

Q: What does this mean for the Bank of Japan's monetary policy path?

A: A prolonged Hormuz shock would complicate the BOJ’s policy path. BOJ Governor Ueda has already warned that the conflict could significantly affect Japan through energy prices and financial markets, and BOJ outlook materials explicitly treat crude oil prices as an important input to the inflation outlook. A sustained energy shock could lift headline inflation while also weighing on growth and household purchasing power. That combination would not mechanically imply either tighter or looser policy, but it would increase policy uncertainty and likely reinforce the BOJ’s preference for caution.

Q: Could Japan deploy its Self-Defense Forces to the Strait of Hormuz?

A: Japan could continue or expand non-combat information-gathering activities in and around the region under the kind of framework it has used since 2019. A more forceful deployment, especially minesweeping or operations connected to collective self-defense, would be much more legally and politically difficult. Japan’s security legislation provides for action in a survival-threatening situation, but whether a Hormuz crisis meets that threshold would be a live government determination, not an automatic outcome. The legal basis exists for some forms of deployment, but the threshold for combat-related or coalition-linked operations is much higher.

Photo Credits

Crude oil, condensate, and petroleum products transported through the Strait of Hormuz in 2014 through 2018 (48097472312) (cropped)

By U.S. Energy Information Administration - Crude oil, condensate, and petroleum products transported through the Strait of Hormuz in 2014 through 2018, Public Domain, https://commons.wikimedia.org/w/index.php?curid=79834249